On May 19, the SEC proposed two sets of rule and form amendments that would implement significant changes to the registered offering and public company reporting frameworks.

Registered Offering Reform

- Form S-3 Eligibility: Removes the 12-month Exchange Act reporting requirement and eliminates all transaction requirements, including the $75 million public float threshold for unlimited shelf offerings. Issuers would still need to be current and timely in their Exchange Act reporting. The SEC estimates this could increase the number of issuers eligible for unlimited Form S-3 offerings by over 60%.

- WKSI-Style Benefits Extended: Enhanced registration and communication flexibilities (currently limited to WKSIs with a $700-plus million public float or $1-plus billion in registered debt) would be available to any issuer eligible to use Form S-3 with at least one class of common equity listed on a national exchange. Use of automatic shelf registration statements would still require 12 months of Exchange Act reporting. Estimated 200% or more increase in eligible issuers.

- State Law Preemption: Defines "qualified purchaser" under § 18(b)(3) of the Securities Act to preempt state blue sky registration and qualification requirements for all registered offerings, including unlisted securities.

- Form S-1 Incorporation by Reference: Permits backward incorporation regardless of whether the issuer has filed an annual report for its most recent fiscal year, and forward incorporation regardless of SRC status. Estimated up to 106% increase in issuers eligible to forward incorporate.

Filer Status and EGC Accommodations Reform

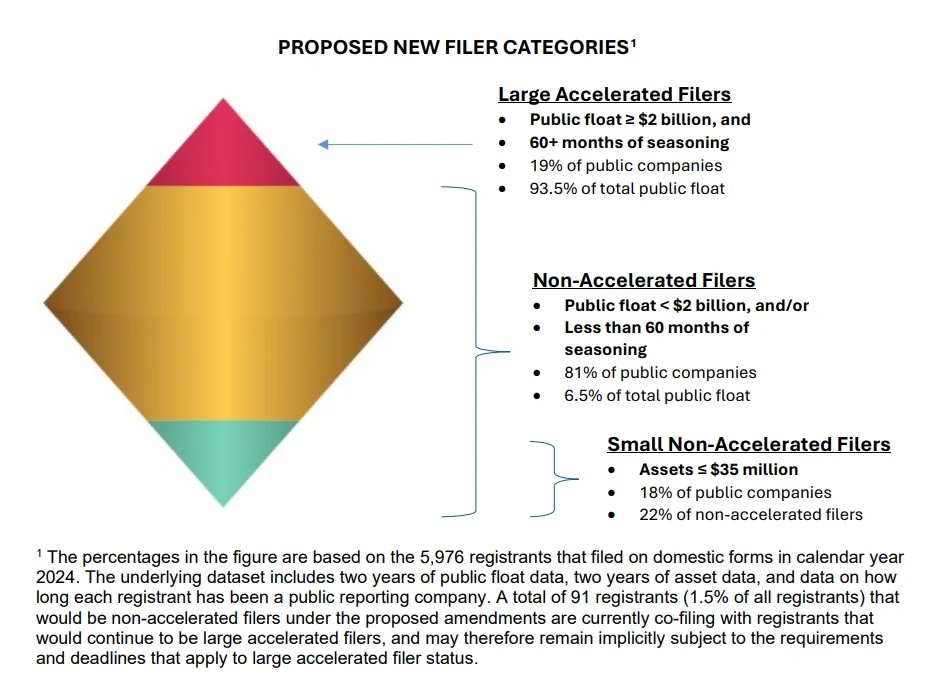

- Large Accelerated Filer (LAF) Threshold Raised to $2 Billion: Public float threshold increases from $700 million to $2 billion, calculated based on the average stock price over the last 10 trading days of the second fiscal quarter, and must be met for two consecutive years.

- "IPO On-Ramp": A company cannot become a LAF until it has at least 60 consecutive months (in other words, five years) of reporting history, regardless of public float.

- Simplified Filer Categories: Eliminates the accelerated filer and smaller reporting company categories. All non-LAFs become non-accelerated filers (NAF) and would be exempt from the ICFR auditor attestation requirement.

- Extended Scaled Disclosure and Accommodations: All NAFs would receive disclosure scaling and accommodations currently available to SRCs and EGCs, including no say-on-pay/say-when-on-pay votes, scaled executive compensation disclosure (including no pay versus performance), and fewer years of financial statements (with reduced presentation requirements.

- Small Non-Accelerated Filer Subcategory: Companies with total assets of $35 million or less for the two most recent years would receive an additional 30 days to file Form 10-K and an additional five days to file Form 10-Q. The graphic below summarizes the new categories.

Image

SEC

- Estimated Impact: Under the proposal, approximately 19% of current public companies would be LAFs (down from 35%) and 81% would be NAFs. Approximately, 18% of public companies would qualify as small non-accelerated filers.

Next Steps

- Both proposals are subject to a 60-day public comment period following publication in the Federal Register.

| Read Fenwick's client alert, "SEC Proposes Broader Offering Flexibility and Simplified Reporting Requirements for Public Companies," for more details. |